Securing financing is often a critical step for small business growth. Private loans, distinct from traditional bank loans, offer a variety of options tailored to diverse business needs.

This comprehensive guide will walk you through the process of obtaining small business loans from private lenders, emphasizing understanding your business, defining goals, and preparing a compelling application.

Understanding Your Business and Needs

Before you embark on the journey to secure a small business loan, it’s essential to have a thorough understanding of your business and its needs. This involves evaluating your business’s current state, market position, and future prospects.

Start by conducting a SWOT analysis (Strengths, Weaknesses, Opportunities, and Threats). This analysis will help you pinpoint areas where funding could be most beneficial. For instance, if your business is expanding, you might need an equipment financing loan to enhance production capabilities.

Defining Your Business Goals

Clear, well-defined business goals are crucial when seeking private loans for small businesses. Start by identifying your short-term and long-term objectives. Whether you plan to increase inventory, invest in new technology, or open a new location, your goals will determine the type of financing you need.

Specific goals enable you to communicate your requirements effectively to potential lenders. For example, if you’re planning to launch a new product line, an equipment financing loan might be appropriate to purchase the necessary machinery.

Assessing Your Financial Health

A comprehensive assessment of your financial health is fundamental to securing a small business loan. Review your financial statements, including balance sheets, income statements, and cash flow statements. This assessment will help you determine how much funding you require and your capacity to manage and repay the loan.

Key financial metrics to evaluate include profit margins, operating expenses, and revenue trends. Understanding these elements will provide a clearer picture of your financial health and help you present a robust case to lenders.

Identifying Funding Requirements

With a clear grasp of your business needs and goals, the next step is to identify your specific funding requirements. Determine the total amount of money you need and the purpose of each portion of the funding. For example, if you’re considering equipment financing, specify the equipment you intend to purchase and its role in your business operations.

Breaking down your funding needs into categories such as operational expenses, capital expenditures, and working capital will help you create a precise loan request and make it easier for business loan lenders to understand your requirements.

Exploring Private Lending Options

Private lenders offer a range of financing options for small businesses. These options often provide more flexibility compared to traditional banks. Here are some common types of private loans you might consider:

Short-Term Loans for Small Businesses:Â These loans, typically with a repayment period of one year or less, are ideal for businesses needing quick access to cash for immediate expenses.

Equipment Financing Loan:Â Designed specifically for purchasing or leasing equipment, this type of loan helps businesses acquire necessary machinery without depleting working capital.

Merchant Cash Advances:Â This option provides a lump sum of cash in exchange for a percentage of future sales or daily credit card transactions, offering immediate capital based on your revenue.

Business Lines of Credit: A line of credit provides flexibility, allowing you to borrow up to a certain limit and only pay interest on the amount you use. It’s particularly useful for managing cash flow fluctuations.

Invoice Financing:Â If you have outstanding invoices, you can secure funding by using those invoices as collateral. This option helps improve cash flow by advancing funds against pending payments.

Benefits of Business Loan Lenders

Private lending offers numerous advantages for small businesses:

Flexibility:Â Private lenders often provide more flexible terms and conditions compared to traditional banks. This can include customized repayment schedules and loan structures tailored to your business needs.

Faster Approval:Â The approval process for private loans can be quicker, allowing you to access funds more rapidly. This is especially beneficial if you need immediate capital to address urgent business needs.

Tailored Solutions:Â Private lenders may offer tailored financing solutions based on your specific business requirements. This personalized approach can help you secure the exact type of loan that aligns with your goals.

Building a Strong Loan Application

A well-prepared loan application can significantly enhance your chances of securing funding. Follow these steps to build a strong application:

Craft a Compelling Business Plan:Â Your business plan should provide a comprehensive overview of your business, including its mission, vision, and objectives. It should also detail how the loan will contribute to achieving these goals.

Develop Financial Projections:Â Prepare detailed financial projections, including cash flow statements, profit and loss forecasts, and balance sheets. These projections should demonstrate your ability to manage and repay the loan effectively.

Prepare Essential Documentation:Â Gather all necessary documentation, such as tax returns, financial statements, and business licenses. Ensure that all documents are accurate and up-to-date to facilitate a smooth application process.

Showcase Your Business Achievements:Â Highlight any significant achievements, milestones, or successes your business has experienced. This can help build credibility and illustrate the potential for growth and success.

Crafting a Compelling Business Plan

A compelling business plan is a crucial element of your loan application. Include the following sections:

Executive Summary:Â Provide a concise overview of your business, including its mission, vision, and strategic goals.

Market Analysis:Â Analyze your industry, target market, and competitive landscape. Demonstrate your understanding of market trends and opportunities.

Marketing and Sales Strategy:Â Outline your strategies for acquiring and retaining customers. Detail your marketing channels, sales tactics, and customer engagement plans.

Operations Plan: Describe your business’s operational processes, including production, distribution, and customer service.

Management Team:Â Introduce your management team, highlighting their relevant experience and roles within the company.

Developing Financial Projections

Detailed financial projections are essential for demonstrating your business’s financial health and ability to repay the small business loan. Include:

Revenue Projections:Â Estimate your expected revenue based on market research and historical data.

Expense Forecasts:Â Outline your anticipated expenses, including both fixed and variable costs.

Cash Flow Projections:Â Provide a cash flow statement that shows how you plan to manage cash inflows and outflows.

Break-Even Analysis:Â Calculate the point at which your business will cover its expenses and become profitable.

Preparing Essential Documentation

Organizing and preparing your documentation is key to a successful loan application. Essential documents include:

Business Financial Statements:Â Provide recent balance sheets, income statements, and cash flow statements.

Tax Returns:Â Include personal and business tax returns for the past few years.

Business Licenses and Permits:Â Ensure that you have all necessary licenses and permits for operating your business.

Legal Documents:Â Include any legal documents related to your business structure, such as partnership agreements or articles of incorporation.

Collateral Documents:Â If applying for a secured loan, provide documentation for the assets you plan to use as collateral.

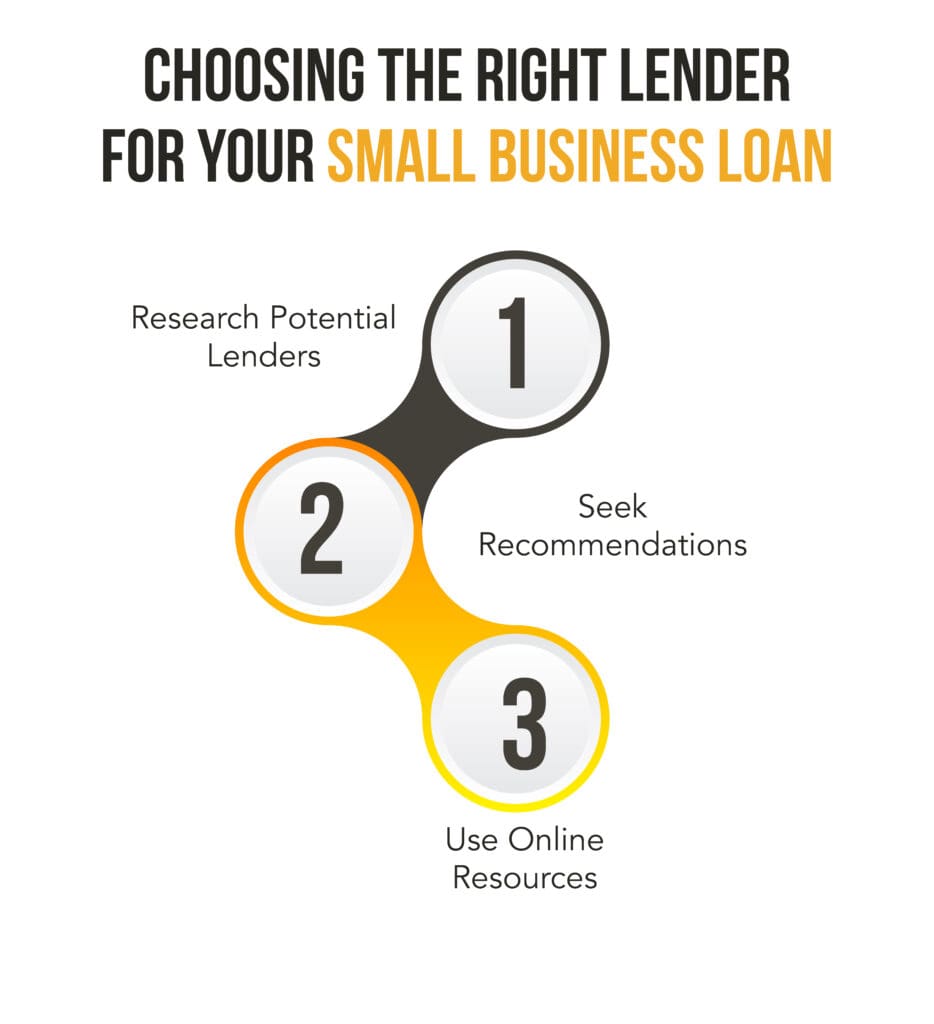

Finding A Small Business Loans Lender

The first step in securing a small business loan is finding the right lender. Private lenders vary widely in terms of their offerings, processes, and requirements, so it’s crucial to identify one that aligns with your business’s needs.

Research Potential Lenders: Begin by researching various private lenders. These can include venture capitalists, private equity firms, peer-to-peer lending platforms, and specialized lending companies. Each type of lender has its own set of criteria and loan products, so understanding these will help you narrow down your options.

Seek Recommendations: Leverage your network to get recommendations. Fellow business owners, financial advisors, or industry contacts can provide insights and refer you to reputable lenders. Their experiences can guide you in choosing a small business lender that suits your business needs.

Use Online Resources: Explore online platforms and marketplaces that connect businesses with private lenders. Websites like Fundera, LendingTree, and other loan marketplaces offer tools to compare various loan products and lenders, making it easier to find a suitable option.

Networking and Building Relationships

Networking and building relationships with potential lenders can enhance your chances of securing a loan. Establishing a strong rapport with lenders can provide several advantages:

Attend Industry Events: Participate in industry conferences, trade shows, and networking events where you can meet potential lenders and investors. These events offer opportunities to make personal connections and discuss your business needs.

Engage with Professional Associations: Join business associations and chambers of commerce. These organizations often have connections with private lenders and can provide valuable introductions and recommendations.

Build a Strong Online Presence: Maintain an active presence on professional networking sites like LinkedIn. Engage with industry groups and connect with potential lenders to build relationships and establish credibility.

Online Platforms and Marketplaces

Online platforms and marketplaces have revolutionized the lending landscape, making it easier for small businesses to find and secure loans. Here’s how to effectively use these platforms:

Read Reviews and Ratings: Check reviews and ratings of lenders on these platforms. Customer feedback can provide insights into the lender’s reliability, customer service, and overall satisfaction.

Leverage Pre-Qualification Tools: Many online platforms offer pre-qualification tools that let you gauge your eligibility for different loans without impacting your credit score. Use these tools to narrow down your options and identify lenders who are likely to approve your application.

Due Diligence: Researching Potential Lenders

Conducting thorough due diligence is essential before committing to a lender. This step helps ensure that you choose a reputable lender and avoid potential issues:

Verify Lender Credentials: Check the credentials and background of potential lenders. Verify their registration, licensing, and regulatory compliance. This can help avoid scams and ensure you’re dealing with a legitimate lender.

Evaluate Lender Reputation: Research the lender’s reputation in the industry. Look for any red flags, such as customer complaints, legal disputes, or negative reviews. A reputable lender will have a track record of fair and transparent dealings.

Assess Customer Support: Evaluate the lender’s customer support services. Effective communication and support can be crucial during the loan application process and throughout the life of the loan.

Negotiation and Closing the Deal

Once you’ve identified a suitable lender, the next step is negotiating and closing the deal. This process involves several key considerations:

Understand Loan Terms and Conditions: Carefully review the loan terms and conditions offered by the lender. This includes the interest rate, repayment schedule, loan term, and any fees or charges. Ensure you fully understand the terms before proceeding.

Negotiate Favorable Rates: Negotiate with the lender to secure the best possible interest rates and repayment terms. Leverage your research and market comparisons to negotiate more favorable conditions.

Review Legal Documents: Before signing any agreements, review all legal documents carefully. Consider consulting with a legal advisor to ensure that all terms are clear and there are no unfavorable clauses.

Closing the Loan and Disbursement

After finalizing the terms and agreements, you’ll proceed to close the loan and receive the funds. Here’s what to expect:

Finalize Documentation: Complete any remaining paperwork required by the lender. This may include providing additional documentation or fulfilling any preconditions set by the lender.

Disbursement of Funds: Once the loan is closed, the lender will disburse the funds. This can be done through a lump sum payment or multiple installments, depending on the loan structure and your agreement.

Confirm Receipt: Verify that you have received the funds and that they have been deposited into your business account. Ensure that the amount matches the agreed-upon loan amount.

Post-Loan Management and Growth

Effective management of the loan post-disbursement is crucial for ensuring that the funds contribute to your business’s growth. Here’s how to manage the loan effectively:

Effective Use of Loan Proceeds: Use the loan funds for their intended purpose, whether it’s for equipment financing, expanding operations, or other business needs. Proper allocation of funds can help maximize the benefits of the loan.

Monitor Financial Performance: Keep a close eye on your business’s financial performance. Regularly review financial statements, cash flow, and operational metrics to ensure that the loan is positively impacting your business.

Communicate with the Lender: Maintain open communication with your lender. If you encounter any issues or changes in your financial situation, inform the lender promptly. This can help you manage any potential challenges and maintain a positive relationship.

Building a Strong Financial Foundation

A strong financial foundation is essential for long-term business success and future funding opportunities:

Maintain Accurate Records: Keep detailed and accurate financial records. This includes tracking income, expenses, and loan repayments. Proper record-keeping helps in managing your finances and preparing for future funding rounds.

Develop a Budget: Create and adhere to a budget that aligns with your business goals. A well-planned budget helps manage expenses, allocate resources efficiently, and ensure that loan repayments are made on time.

Build Reserves: Establish a financial reserve or contingency fund. This can provide a safety net for unexpected expenses and help maintain financial stability.

Preparing for Future Funding Rounds

Preparing for future funding rounds involves several key steps:

Review and Update Business Plan: Regularly review and update your business plan to reflect any changes in your business strategy, goals, or market conditions. A current business plan is essential for attracting future investors or lenders.

Strengthen Financial Health: Focus on improving your financial health by increasing revenue, reducing costs, and optimizing cash flow. Strong financial performance can enhance your attractiveness to potential lenders or investors.

Build Investor Relationships: Cultivate relationships with potential investors or lenders for future funding needs. Networking and maintaining connections with industry professionals can help you access additional funding when required.

Common Pitfalls to Avoid

To ensure a smooth loan application and management process, avoid these common pitfalls:

Lack of Preparation: Failing to thoroughly prepare for the loan application process can lead to delays and potential rejections. Ensure that you have all necessary documentation and a clear understanding of your financial needs.

Ignoring Loan Terms: Overlooking loan terms and conditions can result in unexpected costs or unfavorable terms. Carefully review and negotiate terms to secure the best deal for your business.

Inadequate Financial Management: Poor financial management can negatively impact your ability to repay the loan and manage your business effectively. Implement sound financial practices and maintain accurate records.

Legal and Tax Implications

Understanding the legal and tax implications of taking out a loan is essential:

Legal Considerations: Consult with a legal advisor to ensure that all loan agreements and contracts are legally sound and compliant with applicable regulations. Understanding your legal obligations can prevent potential disputes.

Tax Implications: Be aware of any tax implications related to the loan. Interest payments and other loan-related expenses may have tax consequences. Consult with a tax professional to understand how the loan affects your tax situation.

Leveraging Technology for Loan Management

Technology can play a crucial role in managing your loan and overall financial health:

Use Financial Management Software: Leverage financial management software to track expenses, monitor cash flow, and manage loan repayments. These tools can provide valuable insights and help you stay on top of your financial obligations.

Automate Payments: Set up automated loan payments to ensure timely repayments and avoid late fees. Automating payments can also help manage cash flow and reduce administrative overhead.

Monitor Performance with Analytics: Use analytics tools to track your business performance and assess the impact of the loan. Data-driven insights can help you make informed decisions and optimize your financial strategy.

Ready to secure the right funding for your business?VIP Capital Funding offers tailored solutions for your needs, from online small business loans to short-term loans and construction loans. Whether you’re seeking a small business loan in Georgia, Illinois, Maryland, Michigan, New Jersey, North Carolina, Ohio, or Virginia, we’ve got you covered.

Explore our diverse loan programs and get the working capital you need. Apply now for fast and easy small business loans!