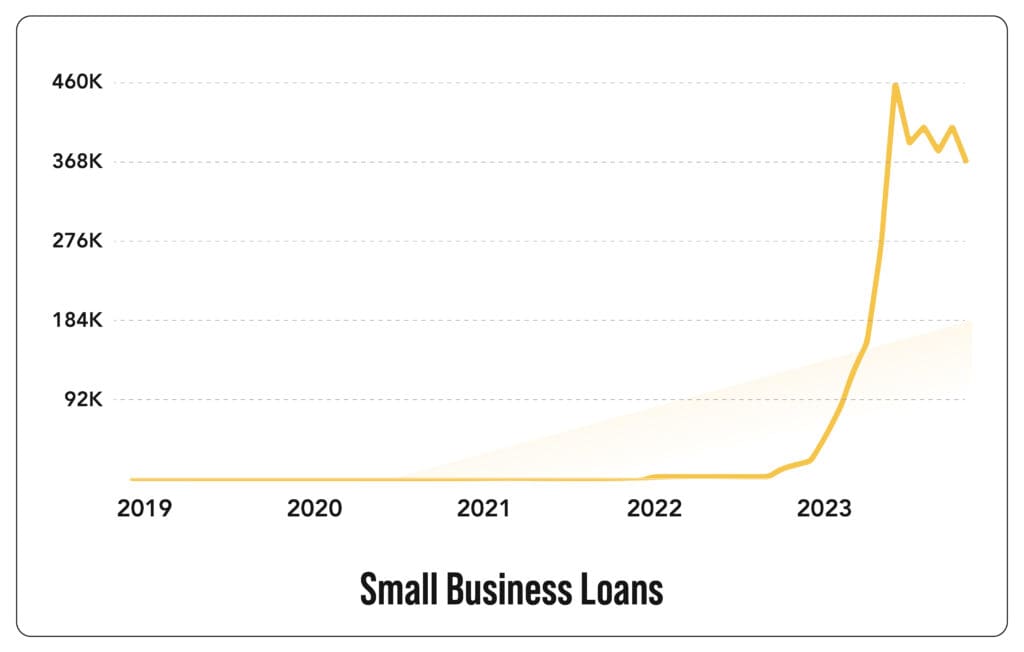

Securing financing is crucial for small business growth, and private loans offer tailored options distinct from traditional bank loans.

Securing financing is crucial for small business growth, and private loans offer tailored options distinct from traditional bank loans.

Short-term business funding is a financial solution designed to provide businesses with quick access to capital for a short period, typically ranging from a few months to a year. Unlike long-term financing, which is structured for extended repayment periods, short-term business funding addresses immediate financial needs, offering a swift injection of cash to help manage operational expenses, seize growth opportunities, or navigate unexpected financial hurdles.

This type of funding can be particularly valuable for small businesses facing seasonal fluctuations in revenue, those looking to capitalize on time-sensitive opportunities, or startups needing initial capital to purchase essential equipment or cover other startup expenses.

When comparing short-term business funding to traditional loans, several key differences stand out.

Short-term business funding can be a game-changer for various reasons:

The landscape of business financing has evolved significantly, with private lenders playing an increasingly prominent role. Unlike traditional financial institutions, private lenders offer a more flexible and personalized approach to funding. This rise in private lending is driven by several factors:

Partnering with a private lender can offer several advantages for businesses seeking short-term funding:

Selecting the right private lender for your short-term business funding needs is crucial to ensuring a positive and productive borrowing experience. Here are some tips for finding the right lender:

Short-term business funding comes in various forms, each suited to different business needs. Here are some common types:

Effectively managing short-term funding is crucial to prevent it from becoming a burden. The first step is to clearly define the purpose of the loan. Is it to cover operational costs, invest in inventory, or seize a time-sensitive opportunity? Once the purpose is clear, it’s essential to calculate the exact amount needed. Overborrowing can lead to unnecessary interest costs, while underborrowing may not fully address the issue.

A well-structured repayment plan is the backbone of successful short-term funding. This plan should be realistic and aligned with your business’s cash flow cycle. Break down the loan amount into manageable installments and determine the payment frequency. Consider using tools like cash flow forecasting to predict income and expenses, ensuring that repayments are sustainable. Regular monitoring of your cash flow will help you stay on top of your repayment schedule.

Strong cash flow management is essential for repaying short-term loans and maintaining business health. Implementing strategies such as:

Invoice discounting:Â Accelerate cash inflow by selling outstanding invoices to a third party at a discount.

Inventory management:Â Optimize stock levels to avoid tying up capital in unsold goods.

Expense control:Â Identify areas where costs can be reduced without compromising business operations.

Pricing strategy:Â Review and adjust pricing to improve profit margins.

Debt collection:Â Implement efficient systems to recover outstanding payments promptly.

Can significantly improve your cash flow position.

While short-term funding can be a valuable tool, it’s essential to avoid becoming reliant on it. Overusing short-term loans can lead to a debt cycle that’s difficult to break. Focus on building a solid financial foundation through improved revenue generation, cost reduction, and efficient cash management. This will reduce your reliance on external financing.

Loan terms and conditions: Carefully review the terms and conditions of the loan agreement, including interest rates, fees, and repayment schedules.

Alternative financing options:Â Explore other financing options such as lines of credit, invoice factoring, or merchant cash advances to find the best fit for your business.

Financial planning:Â Develop a comprehensive financial plan that outlines your business goals, revenue projections, and expense budgets.

Short-term business loans typically come with higher interest rates and fees compared to traditional loans. Understanding these costs is crucial for making informed decisions. Factors such as loan amount, repayment terms, and the lender’s risk assessment influence the overall cost.

Short-term business funding, often accessed through small business loans or other financial products, can be a catalyst for growth and stability when used strategically. Here are some key rewards:

Short-term funding can provide the necessary capital to seize market opportunities, introduce new products or services, or expand into new territories. By injecting funds into key areas, businesses can accelerate their growth trajectory and gain a competitive edge.

One of the most common reasons for seeking short-term business funding is to bridge cash flow gaps. Seasonal fluctuations, unexpected expenses, or slow-paying customers can strain a business’s finances. A small business loan can provide the liquidity needed to meet short-term obligations and maintain operations.

By utilizing short-term funding, businesses can preserve their working capital. This means avoiding the need to liquidate assets or delay critical payments, allowing the business to maintain its operational efficiency and focus on core competencies.

Successful management of short-term funding can contribute to building a strong financial foundation. By demonstrating responsible borrowing and repayment, businesses can improve their creditworthiness and access more favorable financing options in the future. This lays the groundwork for long-term growth and stability.

Short-term business funding can equip businesses with the resources to invest in technology, marketing, or employee training. These investments can enhance competitiveness, improve efficiency, and ultimately drive sales and profitability.

By understanding and leveraging these rewards, businesses can make informed decisions about whether short-term funding is the right choice and how to maximize its benefits.

Using short-term funding as a stepping stone to long-term financial stability is ideal. By effectively managing the loan and implementing sound financial practices, businesses can strengthen their creditworthiness and access more favorable financing options in the future. A strong financial foundation is essential for sustainable growth and resilience.

Remember, short-term business funding is a tool, not a solution. By understanding its benefits, risks, and proper management, you can harness its power to drive your business forward while minimizing potential pitfalls.

Short-term business financing can be a lifeline for companies facing temporary cash flow challenges or seeking to capitalize on fleeting opportunities. This type of funding, often in the form of small business loans or lines of credit, can be instrumental in various business scenarios.

Seasonal Fluctuations:Â Businesses with seasonal sales patterns may experience cash shortages during slower periods. Short-term financing can tide them over until revenue picks up.

Unexpected Expenses:Â Unforeseen costs like equipment repairs or legal fees can disrupt cash flow. Short-term funding can provide the necessary liquidity to address these issues.

Delayed Payments:Â Outstanding invoices can strain a business’s cash flow. Short-term financing can help maintain operations while awaiting payments.

New Product or Service Launch:Â Introducing new offerings often requires upfront investments. Short-term financing can fund these initial costs.

Business Expansion:Â Expanding into new markets or locations can be costly. Short-term financing can cover initial expenses.

Inventory Purchases:Â Opportunities to buy inventory at discounts or in bulk can be seized with short-term financing.

Hiring:Â Expanding the workforce to meet increased demand may require upfront costs. Short-term financing can cover these expenses.

Equipment Purchases:Â Investing in new equipment can improve efficiency. Short-term financing can fund these purchases.

To fully leverage short-term financing:

Plan Carefully:Â Develop a detailed budget and cash flow forecast to determine the exact funding needed.

Prioritize Repayment:Â Create a realistic repayment plan to avoid accumulating unnecessary interest.

Explore Alternatives:Â Consider other financing options like invoice factoring or merchant cash advances.

Build Credit: Maintain a good credit score to improve loan terms.

Focus on Long-TermHealth:Â Use short-term financing as a stepping stone to a strong financial foundation.

Short-term business funding is a valuable tool for managing immediate financial needs, supporting growth, and navigating cash flow challenges. By effectively managing your funding, creating a solid repayment plan, and avoiding common pitfalls, you can maximize the benefits of short-term loans for small business and set the stage for long-term success.

Understanding the costs, rewards, and considerations associated with short-term funding helps in making informed decisions and leveraging this financial resource effectively. With careful planning and strategic execution, short-term business funding can be a powerful asset in achieving your business goals and driving future growth.

Looking for reliable funding solutions for your small business? VIP Capital Funding offers tailored small business loans, including short-term loans, construction loans, and working capital options. Whether you’re in New Jersey, North Carolina, Ohio, Pennsylvania, Virginia, Georgia, Illinois, Maryland, Michigan, or Texas, our flexible loan programs are designed to meet your specific needs.

We also provide medical practice financing, equipment financing, and fast funding solutions. Apply online today and discover how VIP Capital Funding can help your business thrive with easy and efficient loan options. Contact us now to get started and unlock your business’s potential!

Securing financing is often a critical step for small business growth. Private loans, distinct from traditional bank loans, offer a variety of options tailored to diverse business needs.

This comprehensive guide will walk you through the process of obtaining small business loans from private lenders, emphasizing understanding your business, defining goals, and preparing a compelling application.

Before you embark on the journey to secure a small business loan, it’s essential to have a thorough understanding of your business and its needs. This involves evaluating your business’s current state, market position, and future prospects.

Start by conducting a SWOT analysis (Strengths, Weaknesses, Opportunities, and Threats). This analysis will help you pinpoint areas where funding could be most beneficial. For instance, if your business is expanding, you might need an equipment financing loan to enhance production capabilities.

Clear, well-defined business goals are crucial when seeking private loans for small businesses. Start by identifying your short-term and long-term objectives. Whether you plan to increase inventory, invest in new technology, or open a new location, your goals will determine the type of financing you need.

Specific goals enable you to communicate your requirements effectively to potential lenders. For example, if you’re planning to launch a new product line, an equipment financing loan might be appropriate to purchase the necessary machinery.

A comprehensive assessment of your financial health is fundamental to securing a small business loan. Review your financial statements, including balance sheets, income statements, and cash flow statements. This assessment will help you determine how much funding you require and your capacity to manage and repay the loan.

Key financial metrics to evaluate include profit margins, operating expenses, and revenue trends. Understanding these elements will provide a clearer picture of your financial health and help you present a robust case to lenders.

With a clear grasp of your business needs and goals, the next step is to identify your specific funding requirements. Determine the total amount of money you need and the purpose of each portion of the funding. For example, if you’re considering equipment financing, specify the equipment you intend to purchase and its role in your business operations.

Breaking down your funding needs into categories such as operational expenses, capital expenditures, and working capital will help you create a precise loan request and make it easier for business loan lenders to understand your requirements.

Private lenders offer a range of financing options for small businesses. These options often provide more flexibility compared to traditional banks. Here are some common types of private loans you might consider:

Short-Term Loans for Small Businesses:Â These loans, typically with a repayment period of one year or less, are ideal for businesses needing quick access to cash for immediate expenses.

Equipment Financing Loan:Â Designed specifically for purchasing or leasing equipment, this type of loan helps businesses acquire necessary machinery without depleting working capital.

Merchant Cash Advances:Â This option provides a lump sum of cash in exchange for a percentage of future sales or daily credit card transactions, offering immediate capital based on your revenue.

Business Lines of Credit: A line of credit provides flexibility, allowing you to borrow up to a certain limit and only pay interest on the amount you use. It’s particularly useful for managing cash flow fluctuations.

Invoice Financing:Â If you have outstanding invoices, you can secure funding by using those invoices as collateral. This option helps improve cash flow by advancing funds against pending payments.

Private lending offers numerous advantages for small businesses:

Flexibility:Â Private lenders often provide more flexible terms and conditions compared to traditional banks. This can include customized repayment schedules and loan structures tailored to your business needs.

Faster Approval:Â The approval process for private loans can be quicker, allowing you to access funds more rapidly. This is especially beneficial if you need immediate capital to address urgent business needs.

Tailored Solutions:Â Private lenders may offer tailored financing solutions based on your specific business requirements. This personalized approach can help you secure the exact type of loan that aligns with your goals.

A well-prepared loan application can significantly enhance your chances of securing funding. Follow these steps to build a strong application:

Craft a Compelling Business Plan:Â Your business plan should provide a comprehensive overview of your business, including its mission, vision, and objectives. It should also detail how the loan will contribute to achieving these goals.

Develop Financial Projections:Â Prepare detailed financial projections, including cash flow statements, profit and loss forecasts, and balance sheets. These projections should demonstrate your ability to manage and repay the loan effectively.

Prepare Essential Documentation:Â Gather all necessary documentation, such as tax returns, financial statements, and business licenses. Ensure that all documents are accurate and up-to-date to facilitate a smooth application process.

Showcase Your Business Achievements:Â Highlight any significant achievements, milestones, or successes your business has experienced. This can help build credibility and illustrate the potential for growth and success.

A compelling business plan is a crucial element of your loan application. Include the following sections:

Executive Summary:Â Provide a concise overview of your business, including its mission, vision, and strategic goals.

Market Analysis:Â Analyze your industry, target market, and competitive landscape. Demonstrate your understanding of market trends and opportunities.

Marketing and Sales Strategy:Â Outline your strategies for acquiring and retaining customers. Detail your marketing channels, sales tactics, and customer engagement plans.

Operations Plan: Describe your business’s operational processes, including production, distribution, and customer service.

Management Team:Â Introduce your management team, highlighting their relevant experience and roles within the company.

Detailed financial projections are essential for demonstrating your business’s financial health and ability to repay the small business loan. Include:

Revenue Projections:Â Estimate your expected revenue based on market research and historical data.

Expense Forecasts:Â Outline your anticipated expenses, including both fixed and variable costs.

Cash Flow Projections:Â Provide a cash flow statement that shows how you plan to manage cash inflows and outflows.

Break-Even Analysis:Â Calculate the point at which your business will cover its expenses and become profitable.

Organizing and preparing your documentation is key to a successful loan application. Essential documents include:

Business Financial Statements:Â Provide recent balance sheets, income statements, and cash flow statements.

Tax Returns:Â Include personal and business tax returns for the past few years.

Business Licenses and Permits:Â Ensure that you have all necessary licenses and permits for operating your business.

Legal Documents:Â Include any legal documents related to your business structure, such as partnership agreements or articles of incorporation.

Collateral Documents:Â If applying for a secured loan, provide documentation for the assets you plan to use as collateral.

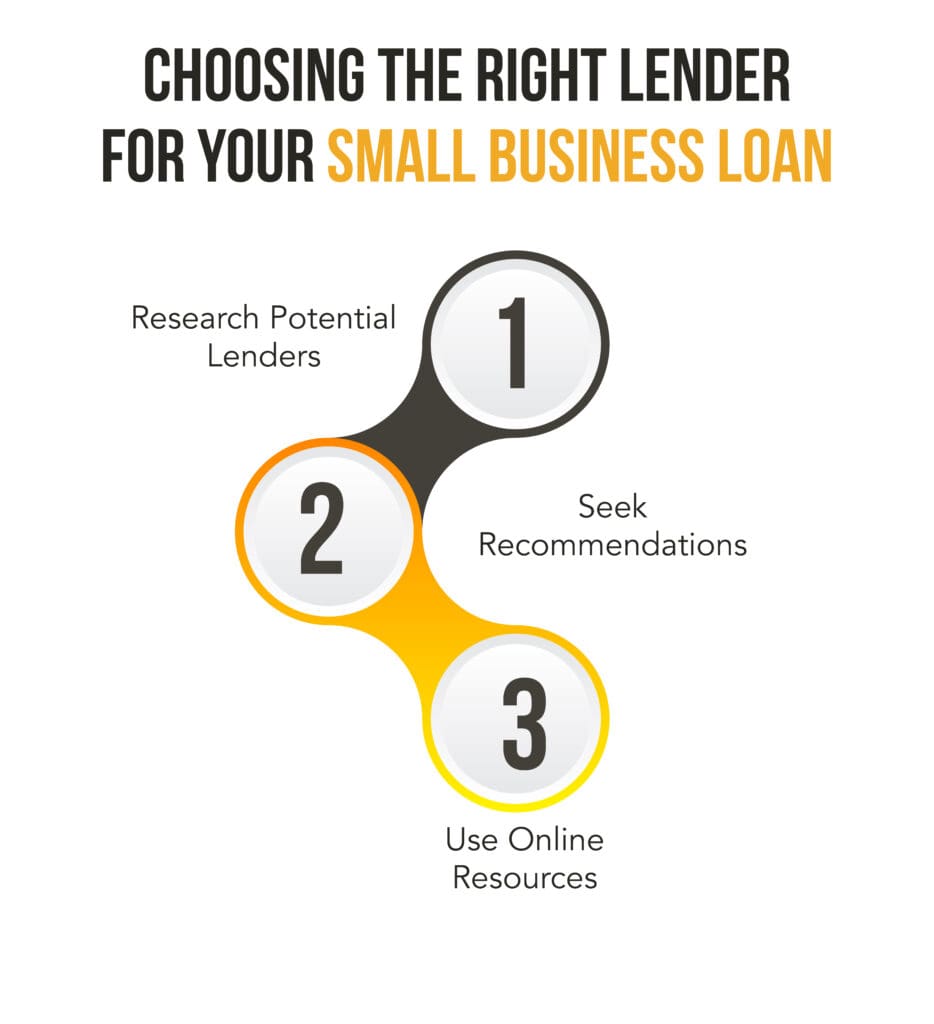

The first step in securing a small business loan is finding the right lender. Private lenders vary widely in terms of their offerings, processes, and requirements, so it’s crucial to identify one that aligns with your business’s needs.

Research Potential Lenders: Begin by researching various private lenders. These can include venture capitalists, private equity firms, peer-to-peer lending platforms, and specialized lending companies. Each type of lender has its own set of criteria and loan products, so understanding these will help you narrow down your options.

Seek Recommendations: Leverage your network to get recommendations. Fellow business owners, financial advisors, or industry contacts can provide insights and refer you to reputable lenders. Their experiences can guide you in choosing a small business lender that suits your business needs.

Use Online Resources: Explore online platforms and marketplaces that connect businesses with private lenders. Websites like Fundera, LendingTree, and other loan marketplaces offer tools to compare various loan products and lenders, making it easier to find a suitable option.

Networking and building relationships with potential lenders can enhance your chances of securing a loan. Establishing a strong rapport with lenders can provide several advantages:

Attend Industry Events: Participate in industry conferences, trade shows, and networking events where you can meet potential lenders and investors. These events offer opportunities to make personal connections and discuss your business needs.

Engage with Professional Associations: Join business associations and chambers of commerce. These organizations often have connections with private lenders and can provide valuable introductions and recommendations.

Build a Strong Online Presence: Maintain an active presence on professional networking sites like LinkedIn. Engage with industry groups and connect with potential lenders to build relationships and establish credibility.

Online platforms and marketplaces have revolutionized the lending landscape, making it easier for small businesses to find and secure loans. Here’s how to effectively use these platforms:

Read Reviews and Ratings: Check reviews and ratings of lenders on these platforms. Customer feedback can provide insights into the lender’s reliability, customer service, and overall satisfaction.

Leverage Pre-Qualification Tools: Many online platforms offer pre-qualification tools that let you gauge your eligibility for different loans without impacting your credit score. Use these tools to narrow down your options and identify lenders who are likely to approve your application.

Conducting thorough due diligence is essential before committing to a lender. This step helps ensure that you choose a reputable lender and avoid potential issues:

Verify Lender Credentials: Check the credentials and background of potential lenders. Verify their registration, licensing, and regulatory compliance. This can help avoid scams and ensure you’re dealing with a legitimate lender.

Evaluate Lender Reputation: Research the lender’s reputation in the industry. Look for any red flags, such as customer complaints, legal disputes, or negative reviews. A reputable lender will have a track record of fair and transparent dealings.

Assess Customer Support: Evaluate the lender’s customer support services. Effective communication and support can be crucial during the loan application process and throughout the life of the loan.

Once you’ve identified a suitable lender, the next step is negotiating and closing the deal. This process involves several key considerations:

Understand Loan Terms and Conditions: Carefully review the loan terms and conditions offered by the lender. This includes the interest rate, repayment schedule, loan term, and any fees or charges. Ensure you fully understand the terms before proceeding.

Negotiate Favorable Rates: Negotiate with the lender to secure the best possible interest rates and repayment terms. Leverage your research and market comparisons to negotiate more favorable conditions.

Review Legal Documents: Before signing any agreements, review all legal documents carefully. Consider consulting with a legal advisor to ensure that all terms are clear and there are no unfavorable clauses.

After finalizing the terms and agreements, you’ll proceed to close the loan and receive the funds. Here’s what to expect:

Finalize Documentation: Complete any remaining paperwork required by the lender. This may include providing additional documentation or fulfilling any preconditions set by the lender.

Disbursement of Funds: Once the loan is closed, the lender will disburse the funds. This can be done through a lump sum payment or multiple installments, depending on the loan structure and your agreement.

Confirm Receipt: Verify that you have received the funds and that they have been deposited into your business account. Ensure that the amount matches the agreed-upon loan amount.

Effective management of the loan post-disbursement is crucial for ensuring that the funds contribute to your business’s growth. Here’s how to manage the loan effectively:

Effective Use of Loan Proceeds: Use the loan funds for their intended purpose, whether it’s for equipment financing, expanding operations, or other business needs. Proper allocation of funds can help maximize the benefits of the loan.

Monitor Financial Performance: Keep a close eye on your business’s financial performance. Regularly review financial statements, cash flow, and operational metrics to ensure that the loan is positively impacting your business.

Communicate with the Lender: Maintain open communication with your lender. If you encounter any issues or changes in your financial situation, inform the lender promptly. This can help you manage any potential challenges and maintain a positive relationship.

A strong financial foundation is essential for long-term business success and future funding opportunities:

Maintain Accurate Records: Keep detailed and accurate financial records. This includes tracking income, expenses, and loan repayments. Proper record-keeping helps in managing your finances and preparing for future funding rounds.

Develop a Budget: Create and adhere to a budget that aligns with your business goals. A well-planned budget helps manage expenses, allocate resources efficiently, and ensure that loan repayments are made on time.

Build Reserves: Establish a financial reserve or contingency fund. This can provide a safety net for unexpected expenses and help maintain financial stability.

Preparing for future funding rounds involves several key steps:

Review and Update Business Plan: Regularly review and update your business plan to reflect any changes in your business strategy, goals, or market conditions. A current business plan is essential for attracting future investors or lenders.

Strengthen Financial Health: Focus on improving your financial health by increasing revenue, reducing costs, and optimizing cash flow. Strong financial performance can enhance your attractiveness to potential lenders or investors.

Build Investor Relationships: Cultivate relationships with potential investors or lenders for future funding needs. Networking and maintaining connections with industry professionals can help you access additional funding when required.

To ensure a smooth loan application and management process, avoid these common pitfalls:

Lack of Preparation: Failing to thoroughly prepare for the loan application process can lead to delays and potential rejections. Ensure that you have all necessary documentation and a clear understanding of your financial needs.

Ignoring Loan Terms: Overlooking loan terms and conditions can result in unexpected costs or unfavorable terms. Carefully review and negotiate terms to secure the best deal for your business.

Inadequate Financial Management: Poor financial management can negatively impact your ability to repay the loan and manage your business effectively. Implement sound financial practices and maintain accurate records.

Understanding the legal and tax implications of taking out a loan is essential:

Legal Considerations: Consult with a legal advisor to ensure that all loan agreements and contracts are legally sound and compliant with applicable regulations. Understanding your legal obligations can prevent potential disputes.

Tax Implications: Be aware of any tax implications related to the loan. Interest payments and other loan-related expenses may have tax consequences. Consult with a tax professional to understand how the loan affects your tax situation.

Technology can play a crucial role in managing your loan and overall financial health:

Use Financial Management Software: Leverage financial management software to track expenses, monitor cash flow, and manage loan repayments. These tools can provide valuable insights and help you stay on top of your financial obligations.

Automate Payments: Set up automated loan payments to ensure timely repayments and avoid late fees. Automating payments can also help manage cash flow and reduce administrative overhead.

Monitor Performance with Analytics: Use analytics tools to track your business performance and assess the impact of the loan. Data-driven insights can help you make informed decisions and optimize your financial strategy.

Ready to secure the right funding for your business?VIP Capital Funding offers tailored solutions for your needs, from online small business loans to short-term loans and construction loans. Whether you’re seeking a small business loan in Georgia, Illinois, Maryland, Michigan, New Jersey, North Carolina, Ohio, or Virginia, we’ve got you covered.

Explore our diverse loan programs and get the working capital you need. Apply now for fast and easy small business loans!

Based on the research, there are new difficulties that are experienced by logistics and supply chain management companies in the modern world which are very dynamic and very competitive in terms of business operation. With the increase in e-commerce and the disruption of global supply chains, many companies have emerged with concerns for optimized and global logistics. Indeed this can only be so as firms have to constantly reinvest in their infrastructure, technology and operation. Nevertheless, such investments are very expensive, and they are an existential problem for many companies and organizations and excluding for SMEs. (more…)

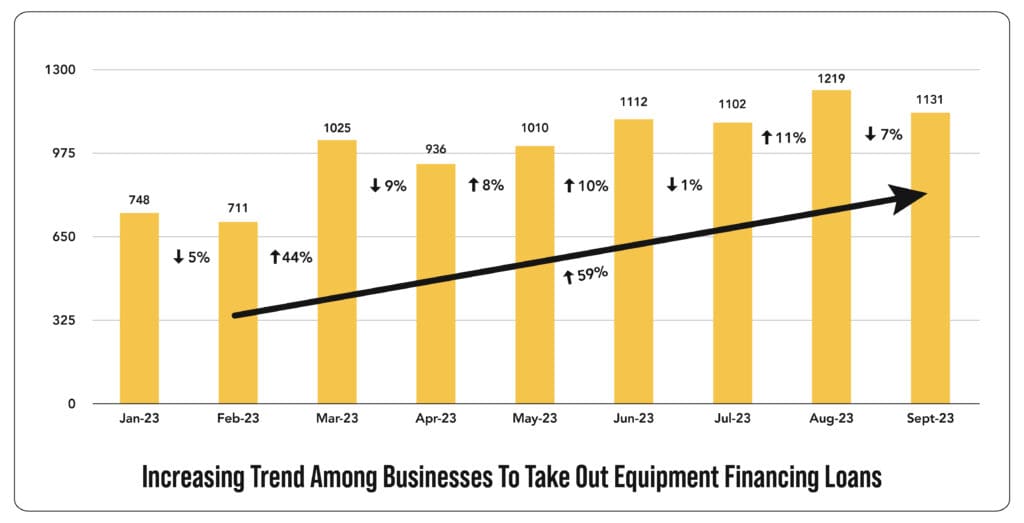

Starting a new business is an exciting endeavor that requires careful planning, strategic decision-making, and, crucially, the right equipment. The importance of equipment in a business cannot be overstated; it is the backbone that supports operations, enhances productivity, and drives growth.

For new businesses, acquiring this essential equipment can be daunting, primarily due to the high costs involved. This is where equipment financing comes into play, providing a viable solution to ease the financial burden and set the stage for success.

The first step in leveraging equipment for business success is identifying what you need. The type of equipment required varies significantly based on the nature of your business and your growth plans. Here’s how to categorize essential equipment:

Identifying your equipment needs involves assessing your current operational requirements and future growth projections. A well-thought-out plan ensures you invest in equipment that aligns with your long-term business goals.

Modern equipment offers several advantages that can significantly impact your business’s efficiency, productivity, and safety.

Investing in modern equipment not only optimizes your current operations but also prepares your business to meet future demands more effectively.

Despite the clear benefits, acquiring new equipment presents significant challenges, especially for new businesses. The most prominent challenge is the financial burden.

Given these challenges, many new businesses turn to equipment financing as a strategic solution.

When it comes to financing equipment, traditional bank loans are often the first option that comes to mind. However, banks can be hesitant to lend to new businesses due to perceived risks. Additionally, bank loans typically involve lengthy approval processes and stringent qualification criteria. This is where alternative financing solutions, such as equipment financing loans from revenue-based private money lenders, become invaluable.

Private money lenders offer a more flexible and accessible financing option compared to traditional banks. These lenders focus on the revenue potential of your business rather than solely relying on credit scores and financial history. Here’s how equipment financing through private money lenders works:

By opting for equipment financing loans from private money lenders, new businesses can access the equipment they need without the hurdles and delays associated with traditional bank loans.

While bank loans have their place, they might not be the best fit for new businesses looking to finance equipment. Here’s why private money lenders are a preferable choice:

By leveraging the flexibility and accessibility of private money lenders, new businesses can overcome the financial barriers of equipment acquisition and set a strong foundation for growth.

One of the most significant advantages of equipment financing is the ability to conserve working capital. This means your cash flow remains available for other crucial business expenses such as marketing, hiring staff, and purchasing inventory. Here’s how it helps:

Equipment financing allows you to acquire the latest technology without the hefty upfront costs. This has several benefits:

Equipment financing can also offer potential tax benefits, which can improve your overall financial health. Here’s how:

These tax advantages make equipment financing an even more attractive option for new businesses looking to optimize their financial strategies.

Choosing the right lender is the first and most crucial step in the equipment financing process. Here are the key factors to consider:

Interest Rates: The interest rate determines the cost of borrowing. Compare rates from different lenders to find the most competitive option. Lower interest rates reduce your overall repayment amount and ease the financial burden on your business.

Loan Terms: Loan terms include the repayment period and schedule. Some lenders offer flexible terms that can be tailored to your cash flow needs, while others may have fixed terms. Evaluate what works best for your business model.

Customer Service Reputation: The lender’s reputation for customer service is important. You want a lender who is responsive, helpful, and supportive throughout the financing process. Check online reviews, ask for referrals, and speak to other business owners who have used the lender’s services.

Specialization in New Businesses: Some lenders specialize in providing equipment financing for new businesses. These lenders understand the unique challenges startups face and may offer more favorable terms and conditions to accommodate them.

A well-prepared financing application increases your chances of approval and can lead to better loan terms. Here’s what you need to do:

Gather Necessary Documents: Collect all the required documents, including business registration papers, personal and business tax returns, bank statements, and proof of business ownership. Some lenders may also require a business plan and financial projections.

Prepare Financial Statements: Financial statements, such as balance sheets, income statements, and cash flow statements, provide lenders with insight into your business’s financial health. Ensure these documents are accurate and up-to-date.

Obtain Equipment Quotes: Get detailed quotes from suppliers for the equipment you intend to purchase. Include specifications, prices, and any warranties or maintenance agreements. Providing this information shows lenders that you have done your homework and are serious about your equipment needs.

Present a Strong Application: Compile all the documents and organize them neatly. Write a cover letter that outlines your business, your equipment needs, and how the financing will help you achieve your goals. Highlight any strong points, such as a solid business plan, experienced management team, or early customer traction.

Once your application is approved, the next step is to negotiate the loan terms and finalize the agreement:

Understand Loan Contracts: Read the loan contract carefully. Ensure you understand all the terms and conditions, including interest rates, repayment schedule, fees, and penalties for late payments or early repayment. If anything is unclear, ask for clarification.

Negotiate Favorable Terms: Don’t be afraid to negotiate. Discuss the interest rate, repayment period, and any fees with the lender. If you have received better offers from other lenders, use them as leverage. Negotiating can save you money and create a more manageable repayment plan.

Secure Funding for Your Equipment: Once you agree on the terms, sign the contract and secure the funding. The lender will disburse the funds directly to the equipment supplier or to your business account, depending on the agreement.

Acquiring equipment is just the beginning. Effective management of your equipment is crucial to maximizing its lifespan and ensuring it contributes to your business’s success.

Preventative maintenance is essential to minimize downtime and extend the lifespan of your equipment. Here’s how to develop an effective schedule:

Regular Inspections: Conduct regular inspections to identify any potential issues early. Check for wear and tear, leaks, or any signs of malfunction.

Scheduled Servicing: Follow the manufacturer’s recommendations for servicing your equipment. This may include routine checks, lubrication, part replacements, and software updates.

Record Keeping: Maintain detailed records of all maintenance activities. Include dates, descriptions of the work done, and any parts replaced. This information is valuable for tracking the equipment’s history and planning future maintenance.

Monitoring your equipment’s performance helps identify opportunities for optimization and cost savings. Here’s what you need to do:

Utilize Performance Metrics: Track key performance metrics such as uptime, output, energy consumption, and efficiency. Use these metrics to assess how well your equipment is performing and identify any areas for improvement.

Implement Monitoring Systems: Use monitoring systems or software to collect real-time data on equipment performance. These systems can alert you to any anomalies or issues, allowing for quick intervention.

Analyze Data for Insights: Regularly analyze the performance data to gain insights into your equipment’s operation. Look for patterns or trends that indicate potential problems or opportunities for optimization.

As your business grows, your equipment needs will evolve. Planning for future equipment acquisition is essential for sustained growth. Here’s how to do it:

Project Future Growth Requirements: Assess your business’s growth projections and determine what additional equipment you will need to support that growth. Consider factors such as increased production capacity, new service offerings, or expansion into new markets.

Align Financing Strategy with Growth Plans: Ensure your financing strategy supports your long-term equipment acquisition plans. Consider setting up a revolving credit line or negotiating flexible terms with your lender to accommodate future purchases.

Stay Informed About Industry Trends: Keep up-to-date with industry trends and technological advancements. Staying informed will help you identify new equipment that could improve your operations or give you a competitive edge.

Easy equipment financing simplifies the process of obtaining funds for essential business equipment. VIP Capital Funding focuses on your revenue rather than credit score, allowing businesses with scores as low as 590 to qualify, provided they meet our revenue criteria of at least $50K monthly or $600K annually.

VIP Capital Funding bases 80% of its decision on your business’s revenue, with only 10% on credit scores and 10% on industry. This approach contrasts with traditional banks, which heavily weigh credit scores and tax returns, enabling quicker approvals and funding for businesses.

Advantages include flexibility in qualification, preservation of working capital, access to modern equipment, and potential tax benefits. Our revenue-based model ensures that even businesses with lower credit scores can secure the necessary funding to grow.

Requirements include generating at least $50K monthly or $600K annually, basic financial documentation, a minimum credit score of 590, and details about your business industry. These criteria ensure a thorough but flexible assessment process.

Ensure your financial statements are accurate, highlight your revenue, provide detailed equipment quotes, gather all necessary documents, and present a well-organized application. Emphasizing these key aspects will increase your chances of securing financing.

Unlock the potential of your business with VIP Capital Funding! Apply for small business loans tailored to your needs, whether you’re in California, Florida, Texas, or beyond. Our easy equipment financing and working capital loans offer quick access to funds, perfect for manufacturers, medical practices, and construction companies. Enjoy fast small business loans, short-term business funding, and specialized financing options in Georgia, Illinois, Maryland, Michigan, New Jersey, North Carolina, Ohio, Pennsylvania, Virginia, and Washington.

Apply for an online small business loan today and propel your business to new heights with our flexible and efficient financing solutions.

Starting or expanding a medical practice can be a challenging yet rewarding endeavor. One of the critical components of ensuring your practice’s success is securing adequate financing.

In this comprehensive guide, we will delve into small business loans for medical practices, explore the different types of loans available, and provide detailed insights on how to navigate the application process.

Medical practice business loans are financial products designed to help healthcare providers manage the operational, expansion, and equipment costs associated with running a medical practice. These loans are tailored to meet the unique needs of medical professionals, offering flexible terms and conditions to support everything from purchasing state-of-the-art medical equipment to expanding office space or covering working capital needs.

Medical practice financing is essential for various reasons, including:

Securing a business loan for a medical practice involves several steps, each crucial to ensuring you get the financing you need on favorable terms. Here’s a detailed look at the process:

Before you begin your search for small business loans for your medical practice, it’s essential to have a clear understanding of your financing needs. Consider the following:

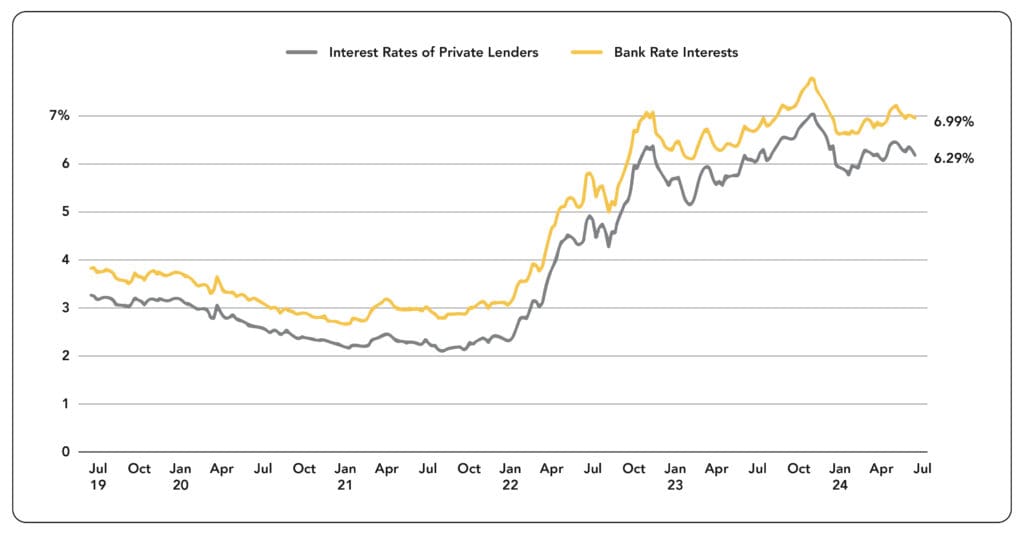

While traditional bank loans and SBA loans are commonly known, they may not always be the best fit for medical practices. Here’s why you might want to consider private money lenders instead:

The documentation required for a medical practice loan can vary depending on the lender and the type of loan. Common documents include:

When searching for the right lender, focus on those specializing in medical practice financing. Here are some tips for comparing lenders:

Once you’ve chosen a lender, it’s time to submit your application. Ensure you provide all the required documentation and information accurately. Be prepared to answer questions about your practice’s operations, financial health, and how you plan to use the loan proceeds.

Medical practice financing can be categorized into several types of loans, each serving different needs. Let’s explore two primary types: traditional bank loans and private money lending loans.

Traditional bank loans are often the first option considered by many business owners. However, they may not always be the best fit for medical practices. Here’s why:

Private Money Lending Loans

Private money lending loans present a compelling alternative to traditional bank loans. Here’s why they are often the preferred choice for medical practices:

Navigating the application process for a medical practice loan involves several critical steps. Here’s a detailed look at what you need to do:

Pre-qualification is an initial step that helps you understand your borrowing capacity without affecting your credit score. During this stage, you’ll typically provide basic information about your practice and your financing needs. The lender will review this information to give you an estimate of the loan amount you may qualify for.

Assemble all necessary documentation before you apply. This includes:

With your documents ready, submit your loan application to the chosen lender. Ensure all information is accurate and complete to avoid delays. Some lenders may offer online application portals, making the process more convenient.

Once submitted, the lender will review your application and supporting documents. They may request additional information or clarification. During this stage, be prepared for:

If approved, you’ll receive a loan agreement outlining the terms and conditions of the loan. Review the agreement carefully, paying attention to the interest rate, repayment schedule, fees, and any other terms. Once you sign the agreement, the funds will be disbursed to your account, ready for use.

Medical business loans offer flexibility and can be utilized for various purposes to support and grow your practice. Here are several key areas where these loans can be instrumental:

Medical equipment is often expensive but essential for providing high-quality care. Equipment financing loans can be used to purchase new diagnostic machines, surgical tools, electronic health record systems, and other necessary medical devices. By spreading the cost over several years, you can manage your cash flow more effectively while ensuring your practice is equipped with the latest technology.

Whether you are looking to lease a new office space, purchase an existing building, or even construct a new facility, a small business loan can cover the real estate costs. A well-located, comfortable, and state-of-the-art facility can significantly enhance patient experience and increase your practice’s visibility and reputation.

Day-to-day operations require a steady flow of working capital. This includes salaries, utility bills, supplies, marketing, and other operational expenses. Small business loans for working capital ensure that your practice runs smoothly without financial hiccups, even during slow periods.

If your practice is growing, you may need to expand your current space or renovate it to improve functionality and aesthetics. Loans can fund construction projects, interior design upgrades, and the addition of new rooms or wings to accommodate more patients or new services.

Keeping up with technological advancements is crucial in the medical field. Loans can be used to upgrade your practice management software, electronic health records (EHR) systems, and telemedicine capabilities, ensuring your practice remains competitive and efficient.

Investing in the professional development of your staff can lead to better patient care and increased job satisfaction. Loans can be used to fund continuing education, training programs, and certifications for your medical and administrative staff.

Maintaining a sufficient inventory of medical supplies, pharmaceuticals, and other consumables is critical. Loans can help you purchase these items in bulk, often at a lower cost, ensuring you have the necessary supplies on hand without straining your finances.

Before you apply for a small business loan for your medical practice, there are several important factors to consider:

Understanding the different types of loans available and their terms is essential. Some common loan types include:

Interest rates and fees can significantly impact the overall cost of your loan. Shop around and compare offers from different private money lenders to find the most favorable terms. Be sure to understand any additional fees, such as origination fees, prepayment penalties, and late payment charges.

Consider the repayment terms carefully. A longer repayment period may result in lower monthly payments but higher overall interest costs, while a shorter term can save you money on interest but require higher monthly payments. Choose a repayment plan that aligns with your cash flow and financial projections.

Working with a reputable lender who has experience in providing loans to medical practices can make the process smoother and more reliable. Research potential lenders, read reviews, and seek recommendations from other medical professionals.

Evaluate the financial health of your practice before applying for a loan. Lenders will want to see that your practice is financially stable and capable of repaying the loan. Prepare detailed financial statements, including profit and loss statements, balance sheets, and cash flow statements.

Clearly define the purpose of the loan and how it will benefit your practice. Whether it’s for expansion, equipment purchase, or working capital, having a clear plan will not only help you in the application process but also ensure that the loan is used effectively.

Some loans may require collateral, such as property, equipment, or other assets. Understand the collateral requirements and be prepared to provide the necessary documentation. Ensure that you are comfortable with the risk involved in using your assets as collateral.

The application process for small business loans can be detailed and time-consuming. Be prepared with all necessary documentation, including financial statements, tax returns, business plans, and legal documents. A well-prepared application can expedite the approval process.

Understand how taking on new debt will impact your practice’s credit and financial statements. While we are not focusing on credit scores, it’s essential to be aware that new loans will affect your overall financial profile and future borrowing capacity.

There are several types of small business loans available for medical practices, including term loans, equipment financing loans, lines of credit, and working capital loans. Each type of loan has its specific use cases and benefits, depending on your practice’s needs.

An equipment financing loan can be used to purchase medical equipment, such as diagnostic machines, surgical tools, and electronic health record systems. The equipment itself typically serves as collateral for the loan, making it a cost-effective way to upgrade your practice’s technology.

Taking on a small business loan will impact your practice’s financial statements and borrowing capacity. It’s essential to ensure that your practice can manage the loan repayments and that the loan will ultimately contribute to the growth and stability of your practice.

Interest rates and fees vary by lender and loan type. It’s crucial to compare offers from different lenders to find the most favorable terms. Be sure to understand any additional fees, such as origination fees, prepayment penalties, and late payment charges.

Unlock the potential of your business with VIP Capital Funding! Apply for small business loans, business equipment financing, and short-term business funding. We offer easy small business loans in California, Florida, and Texas, including working capital loans and equipment financing loans. Enjoy fast small business loans and online applications tailored for medical practice financing, construction, and manufacturers.

Apply for short-term loans and experience hassle-free financing for your new or existing business today!

For small businesses, maintaining a healthy cash flow is crucial to ensure smooth operations. This is where working capital loans come into play, providing the necessary funds to cover short-term expenses and sustain day-to-day business activities.

This comprehensive guide will explore what working capital loans are, how they work, the reasons for acquiring them, the amount of working capital needed by small businesses, the strategic use of these loans for cash flow management, and some frequently asked questions. Read on!

A working capital loan is a type of short-term loan designed to cover a company’s everyday operational expenses. These expenses might include payroll, rent, utilities, inventory purchases, and other short-term liabilities. Unlike other types of loans that are used for long-term investments or major purchases, working capital loans are specifically tailored to provide the liquidity needed to run daily business operations smoothly.

Working capital loans are particularly beneficial for small businesses that may experience seasonal fluctuations in revenue or have uneven cash flows. By securing a working capital loan, these businesses can bridge the gap between their income and expenses, ensuring they have the necessary funds to continue operating without interruption.

The process of obtaining a working capital loan involves several steps, from application to repayment. Here’s a detailed breakdown of how it works:

Identify Needs: The first step is to determine the exact financial needs of the business. This involves assessing the short-term expenses that need to be covered.

Choose a Lender: Small businesses can choose from various private money lenders who offer working capital loans. It’s essential to compare the terms, interest rates, and repayment options of different lenders to find the best fit.

Prepare Documentation: Most lenders require specific documents to process a loan application. These may include financial statements, bank statements, tax returns, and proof of business ownership.

Submit Application: Once all necessary documentation is gathered, the application can be submitted either online or in person, depending on the lender’s process.

Credit Assessment: Lenders will evaluate the business’s creditworthiness, focusing on its ability to repay the loan. While credit scores are considered, they are not the sole determining factor for approval.

Loan Offer: If the application is approved, the lender will present a loan offer detailing the amount, interest rate, and repayment terms.

Acceptance and Disbursement: Upon accepting the loan offer, the funds are disbursed to the business’s bank account. This process can be swift, with some lenders providing funds within a few days.

Repayment terms for working capital loans vary based on the lender and the specific loan agreement. Generally, these loans are short-term, with repayment periods ranging from a few months to a couple of years. Repayment can be structured in various ways, including:

FixedMonthly Payments: Equal payments made each month.

Weekly or Bi-weekly Payments: Smaller, more frequent payments.

Revenue-based Payments: Payments based on a percentage of the business’s monthly revenue.

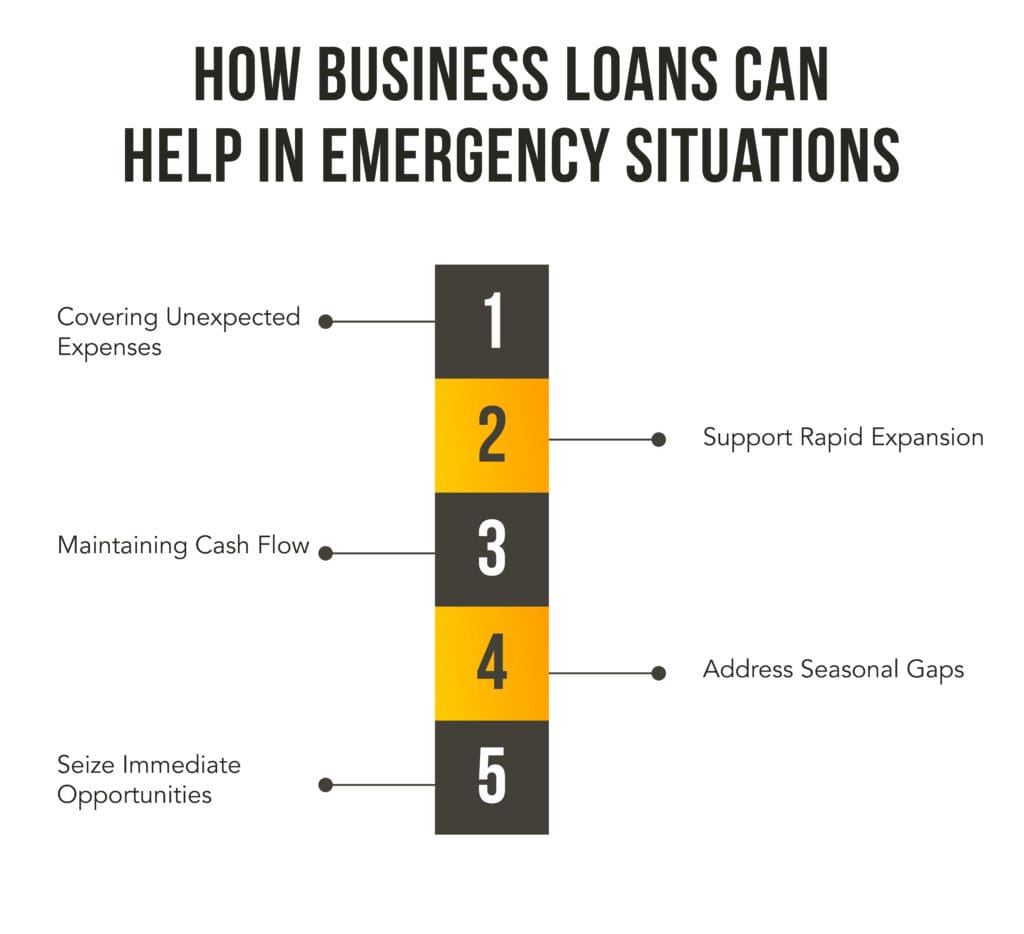

There are several reasons why a small business might seek a working capital loan, including:

One of the primary reasons to get a working capital loan is to manage cash flow effectively. Small businesses often face periods where expenses exceed income, such as during off-peak seasons or when waiting for customer payments. A working capital loan can bridge these gaps, ensuring that bills and payroll are covered without disrupting operations.

Opportunities often arise unexpectedly, and having the financial flexibility to seize them can make a significant difference for small businesses. Whether it’s purchasing discounted inventory, investing in marketing campaigns, or expanding product lines, a working capital loan provides the necessary funds to act swiftly and capitalize on these opportunities.

Unexpected expenses can occur at any time, from equipment breakdowns to sudden increases in supply costs. A working capital loan can provide a safety net to cover these unforeseen costs without straining the business’s finances.

Many small businesses experience seasonal fluctuations in revenue, such as retail stores during holiday seasons or tourism-related businesses during peak travel periods. A working capital loan can help smooth out these fluctuations by providing the funds needed during slower periods to prepare for busy seasons.

Expanding a business will often require significant upfront investments in areas such as new locations, additional staff, or enhanced marketing efforts. A working capital loan can provide the necessary capital to support growth initiatives without depleting the company’s reserves.

Determining the right amount of working capital for a small business depends on several factors, including the nature of the business, industry standards, and specific operational needs. Here are some key considerations:

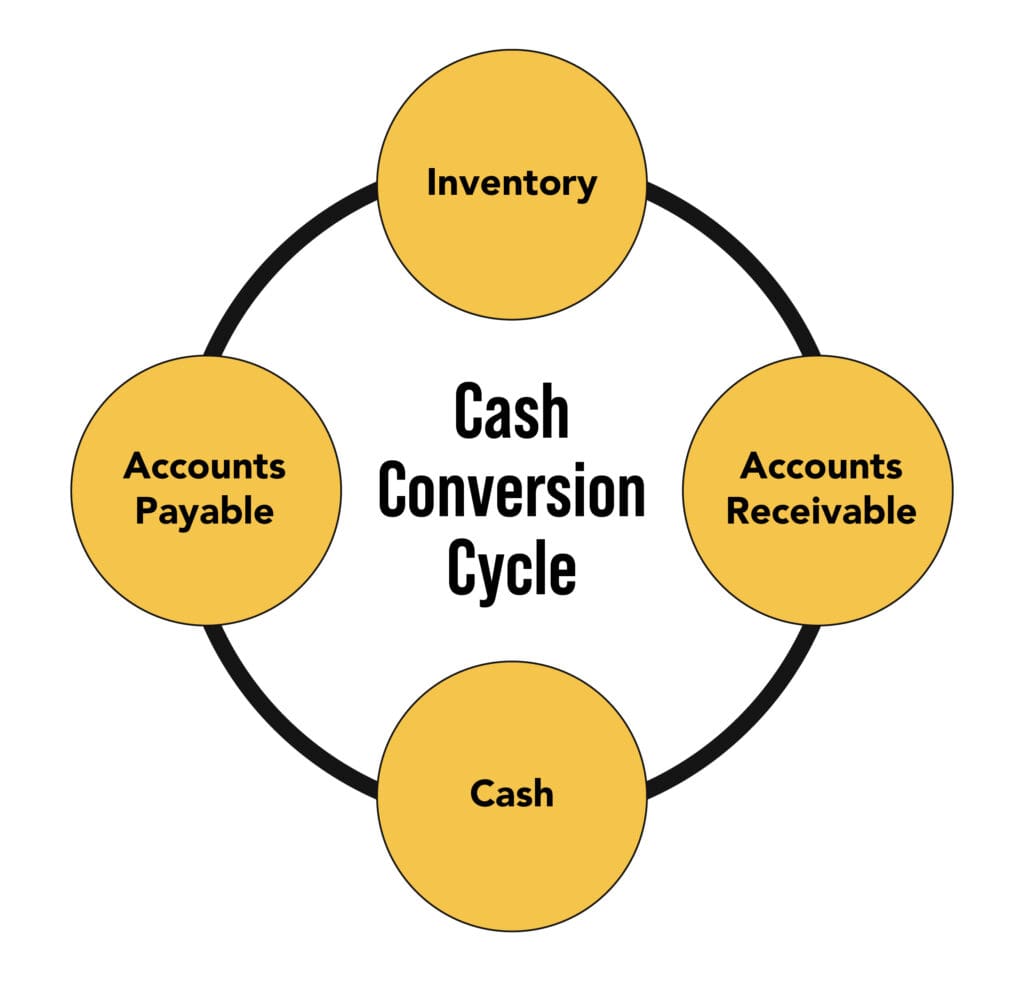

A fundamental step in determining working capital needs is to assess the business’s current assets and liabilities. Current assets include cash, accounts receivable, and inventory, while current liabilities include accounts payable and short-term debts. The difference between current assets and current liabilities is the working capital.

The cash conversion cycle (CCC)Â is a critical metric that measures the time it takes for a business to convert its inventory and other resources into cash flow from sales. The CCC helps determine how much working capital is needed to sustain operations during this period. A longer CCC typically indicates a higher need for working capital.

Different industries have varying working capital requirements based on their operational cycles and business models. Researching industry benchmarks can provide a useful reference point for small businesses to gauge their working capital needs.

Businesses planning for growth or expansion should factor in the additional working capital required to support increased operational demands. This might include higher inventory levels, increased marketing efforts, or additional staff.

For businesses with seasonal fluctuations, it’s essential to plan for the periods when additional working capital will be needed to cover expenses during slower sales cycles. This planning ensures that the business can maintain operations and be ready for peak seasons.

Effectively managing cash flow is critical for the success and sustainability of small businesses. Working capital loans can be a powerful tool in achieving this goal. Here are some strategic ways to use working capital loans to enhance cash flow management:

Maintaining optimal inventory levels is crucial for meeting customer demand without tying up excessive funds in stock. A working capital loan can help small businesses purchase inventory in bulk at discounted rates or stock up on essential items before peak seasons, ensuring they have sufficient inventory to meet customer needs.

Ensuring timely payment of salaries and operational expenses is vital for maintaining employee morale and smooth business operations. Working capital loans can provide the necessary funds to cover payroll and other recurring expenses during periods of low cash flow, preventing disruptions and maintaining employee satisfaction.

Investing in marketing and advertising is essential for business growth and attracting new customers. However, these activities often require significant upfront costs. A working capital loan can provide the funds needed to launch marketing campaigns, enhance brand visibility, and drive sales, ultimately improving cash flow.

Regular maintenance, renovations, and upgrades are necessary to keep a business competitive and appealing to customers. Whether it’s refurbishing a retail space, upgrading equipment, or enhancing the online presence, a working capital loan can fund these improvements without straining the business’s cash reserves.

Many small businesses face challenges with delayed payments from customers, leading to cash flow issues. A working capital loan can bridge the gap between invoicing and payment collection, ensuring that the business has the necessary funds to continue operations while waiting for customer payments.

Suppliers often offer discounts for early payments, which can significantly reduce procurement costs. A working capital loan can provide the liquidity needed to take advantage of these discounts, ultimately improving profit margins and cash flow.

Introducing new products or services can attract more customers and increase revenue. However, developing and launching new offerings require investment in research, development, and marketing. A working capital loan can provide the necessary funds to support these initiatives and drive business growth.

Having access to emergency funds is crucial for small businesses to handle unexpected situations such as natural disasters, economic downturns, or sudden market changes. A working capital loan can serve as a financial cushion, allowing businesses to navigate through challenging times without compromising their operations.

Working capital loans are designed to cover the short-term financial needs of a business. These needs can range from purchasing inventory, covering payroll, paying rent, or handling unexpected expenses. Here’s how these loans can contribute to the growth and stability of your small business:

Cash flow is the lifeblood of any business. Positive cash flow ensures that a business can meet its financial obligations, such as paying suppliers and employees, without disruption. Working capital loans provide a cushion that helps maintain cash flow during slow periods or when facing unexpected expenses. This stability allows business owners to focus on growth rather than constantly worrying about making ends meet.

Opportunities for growth can arise unexpectedly. Whether it’s a chance to buy inventory at a discounted rate, expand to a new location, or invest in marketing to attract more customers, having access to working capital can make all the difference. A working capital loan can provide the funds needed to seize these opportunities without compromising the business’s financial health.

For businesses that rely heavily on inventory, having the right stock at the right time is crucial. Working capital loans can help small businesses purchase inventory in bulk, take advantage of supplier discounts, and ensure they have enough stock to meet customer demand. This not only helps in maintaining customer satisfaction but also improves profitability by reducing per-unit costs.

Many small businesses experience seasonal fluctuations in sales. For instance, a retail business might see higher sales during the holiday season but slower periods during other times of the year. Working capital loans can provide the necessary funds to manage these fluctuations, ensuring that the business can operate smoothly throughout the year. This can include covering expenses during slow periods or ramping up inventory and staffing during peak seasons.

Consistently managing cash flow and meeting financial obligations on time can enhance a business’s creditworthiness. While credit scores aren’t the primary focus here, having a history of successfully repaying loans can make it easier for a business to secure additional financing in the future. This can be beneficial for long-term growth and expansion plans.

Beyond the direct impact on business operations and growth, working capital loans offer several other benefits that make them an attractive financing option for small businesses.

One of the significant advantages of working capital loans is their flexibility. Unlike traditional loans that might be earmarked for specific purposes like purchasing equipment or real estate, working capital loans can be used for a variety of needs. This flexibility allows business owners to allocate funds where they are needed most, whether it’s for daily operations, covering unexpected costs, or investing in growth initiatives.

In the fast-paced world of small business, timing is everything. Working capital loans are often designed to provide quick access to funds, sometimes within days of approval. This rapid turnaround can be crucial when dealing with urgent financial needs or time-sensitive opportunities. Private money lenders, in particular, are known for their ability to expedite the loan process, making them a viable option for businesses that need funds quickly.

Many working capital loans do not require collateral, which can be a significant advantage for small businesses that may not have substantial assets to pledge. Unsecured working capital loans rely on the business’s overall health and cash flow rather than specific assets, making them more accessible to a broader range of businesses.

Unlike equity financing, where business owners have to give up a portion of their ownership in exchange for capital, working capital loans allow owners to retain full control of their business. This means that the business can grow and benefit from the additional capital without diluting ownership or decision-making power.

Working capital loans often come with customizable terms that can be tailored to fit the specific needs of the business. This can include the loan amount, repayment schedule, and interest rates. By working with private money lenders, small business owners can negotiate terms that align with their financial situation and cash flow patterns, making repayment more manageable.

Navigating the world of small business financing can be complex. Here are some frequently asked questions about working capital loans to help clarify any uncertainties.

At VIP Capital Funding, we offer revenue-based funding where credit score is primarily not an issue. We can fund businesses that have relatively lower credit scores, provided they are generating at least $50K annually. For businesses with higher revenues, such as $600K annually or $100K monthly, we can offer more substantial funding options.

Interest rates for working capital loans can vary depending on the lender, the loan amount, and the repayment term. Private money lenders may have higher interest rates compared to traditional banks due to the increased risk they take. However, they often offer more flexible terms and quicker access to funds.

Yes, it is possible to obtain a working capital loan even if you have an existing loan. However, lenders will assess your overall financial health and ability to repay both loans. It’s essential to provide a clear picture of your business’s cash flow and how the new loan will be used to support your operations and growth.

The loan amount you can borrow depends on several factors, including your business’s revenue, cash flow, and the lender’s policies. Private money lenders may offer a wide range of loan amounts, from a few thousand dollars to several hundred thousand dollars, depending on your business needs and qualifications.

While working capital loans are designed to cover short-term operational expenses, they offer significant flexibility in how the funds can be used. You can use the loan for various purposes, including purchasing inventory, covering payroll, paying rent, or investing in marketing and growth initiatives. However, it’s essential to use the funds in a way that supports your business’s financial health and growth.

Unlock your small business’s potential with VIP Capital Funding! Offering fast and flexible financing options like small business loans, equipment financing, and short-term business funding, we cater to businesses in California, Florida, Texas, and beyond. Apply online for easy and quick access to the capital you need to grow and thrive.

From medical practices to construction companies, we have the perfect funding solutions.

Contact us now to get started.

Starting or expanding a small business in Florida requires careful planning and adequate funding. For many entrepreneurs, securing a small business loan is an essential step in this journey. With the variety of loan options available, understanding the intricacies of small business loans in Florida can help you make informed decisions that align with your business goals.

This comprehensive guide will cover key aspects, including understanding small business loans, the benefits they offer, how to determine your loan needs, and the various loan programs available in Florida.

Small business loans are financial products designed to provide capital to businesses that need funding for various purposes, such as startup costs, expansion, purchasing equipment, or managing cash flow. These loans can come from various sources, including private lenders, credit unions, and online lenders. Unlike traditional bank loans, private money loans offer more flexibility and faster approval processes, making them an attractive option for many small business owners.

Identify the specific purpose for which you need the loan. This could be for purchasing new equipment, expanding your business, covering operating expenses, or managing cash flow. Clearly defining the purpose will help you determine the type of loan that best suits your needs.

Calculate the amount of funding required for your specific purpose. Be realistic in your estimation, considering both the immediate and potential future costs. It’s better to ask for a bit more than to find yourself short of funds, but ensure that the amount is justifiable and manageable within your business’s financial structure.

Assess your ability to repay the loan by examining your business’s revenue streams and existing financial obligations. Create a projected cash flow statement to see how loan repayments would fit into your budget. Ensuring that you can comfortably meet the repayment terms is crucial to maintaining your business’s financial health.

Different lenders have varying requirements and terms for their loan products. Research potential lenders to understand their loan criteria, interest rates, repayment terms, and any fees associated with the loan. This will help you choose a lender whose terms align with your business’s financial situation and goals.

Gather the necessary documentation required by lenders. This may include financial statements, tax returns, business plans, and proof of collateral, if applicable. Having your documents organized and ready can expedite the loan application process.

Florida offers various loan programs specifically designed to support small businesses. These programs can provide the funding needed to start or grow your business, purchase equipment, or manage cash flow. Here are some prominent loan programs in Florida:

Business equipment financing is designed to help businesses acquire the equipment they need without a significant upfront investment. This type of financing allows businesses to spread the cost of equipment over time, making it more affordable and manageable. The equipment itself often serves as collateral for the loan, which can make it easier to secure approval.

Preserve Cash Flow: By financing equipment, businesses can preserve their cash flow for other operational needs.

Tax Benefits: In some cases, equipment financing may offer tax benefits, such as the ability to deduct interest payments.

Improved Efficiency: Acquiring the latest equipment can enhance productivity and efficiency, leading to increased profitability.

Loan Terms: Understand the terms of the financing agreement, including the interest rate, repayment schedule, and any associated fees.

Equipment Value: Ensure that the equipment being financed is essential to your operations and will provide a return on investment.

Short-term business funding provides quick access to capital for businesses that need immediate financial support. These loans typically have a shorter repayment period, often ranging from a few months to a year, and are ideal for addressing urgent financial needs or taking advantage of time-sensitive opportunities.

Fast Access to Capital: These loans are often approved and disbursed quickly, providing timely financial support.

Flexibility: Short-term loans can be used for various purposes, including managing cash flow, covering unexpected expenses, or seizing growth opportunities.

Improved Cash Flow: By addressing immediate financial needs, short-term funding can help maintain a steady cash flow.

Higher Interest Rates: Short-term loans often come with higher interest rates compared to long-term loans.

Repayment Terms: Ensure that your business can meet the repayment terms within a short period to avoid financial strain.

The Florida Small Business Emergency Bridge Loan Program provides short-term, interest-free loans to small businesses impacted by a disaster. This program is designed to help businesses bridge the gap between the time of the disaster and the time when long-term recovery funding is secured.

Immediate Relief: Provides quick financial assistance to businesses affected by disasters, helping them recover and resume operations.

Interest-Free: These loans are interest-free, making them a cost-effective option for businesses in need.

Eligibility Requirements: Ensure your business meets the eligibility criteria for the program, such as location and impact of the disaster.

Repayment Terms: Understand the repayment terms and ensure your business can meet the repayment obligations.

The Microfinance Loan Program in Florida is designed to provide small loans to businesses that may not qualify for traditional financing. These loans are typically for smaller amounts and can be used for various business purposes, including working capital, inventory purchase, and equipment acquisition.

Accessibility: Provides funding to small businesses that may have difficulty securing traditional loans.

Flexibility: Funds can be used for a variety of business needs, providing flexibility in how the loan is utilized.

Loan Amount Limits: Microfinance loans are generally for smaller amounts, so ensure the funding is sufficient for your needs.

Lender Terms: Different lenders may have varying terms, so research and compare options to find the best fit for your business.

Private money loans, also known as hard money loans, are provided by private lenders or investors. These loans are typically secured by collateral, such as real estate or business assets, and can be an excellent option for businesses needing quick access to capital or those that may not qualify for traditional financing.

Fast Approval and Funding: Private money loans often have a quicker approval and funding process compared to traditional loans.

Flexible Terms: Private lenders may offer more flexible terms, including interest-only payments or customized repayment schedules.

Less Stringent Requirements: These loans may have less stringent credit requirements, making them accessible to a broader range of businesses.

Higher Interest Rates: Private money loans typically come with higher interest rates due to the increased risk for lenders.

Collateral Requirements: These loans are usually secured by collateral, so ensure you have valuable assets to pledge.

Applying for a small business loan in Florida involves several steps. Here’s a guide to navigating the loan application process:

Start by researching potential lenders and loan programs. Consider factors such as loan terms, interest rates, repayment schedules, and eligibility requirements. Choose a lender and loan product that best aligns with your business’s needs and financial situation.

A well-prepared business plan is essential for demonstrating to lenders that your business is viable and has a clear path to profitability. Include detailed information about your business, market analysis, financial projections, and how the loan will be used.

Collect all the necessary documentation required by the lender. This may include:

Complete the loan application form provided by the lender and submit it along with the required documentation. Ensure that all information is accurate and complete to avoid delays in the approval process.

After submitting your application, follow up with the lender to check the status of your application. Be prepared to provide additional information or clarification if requested.

If your loan application is approved, review the loan offer carefully. Pay attention to the terms and conditions, including the interest rate, repayment schedule, and any fees. If you agree with the terms, accept the offer and proceed with the loan closing process.

Private money lenders in Florida provide a valuable resource for small business owners. These lenders typically offer more flexible terms and faster funding than traditional banks. They often base their lending decisions on the revenue and potential of the business rather than traditional credit scores. This can be particularly advantageous for businesses that have strong cash flows but may not have a long credit history or high credit scores.

Private money lenders often use revenue-based funding models, which focus on the business’s cash flow rather than the owner’s credit history. Here’s how it works:

Revenue Assessment: Lenders look at the business’s monthly or annual revenue to determine loan eligibility and the amount that can be borrowed.

Repayment Terms: Repayment is typically a fixed percentage of the business’s revenue, ensuring that payments are manageable and proportional to the business’s income.

Flexible Requirements: Since the loan is secured against future revenues, lenders are more flexible regarding traditional collateral requirements.

While private money lenders are more flexible, there are still some common eligibility criteria:

Business Age and Revenue: Lenders usually prefer businesses that have been operational for a certain period (e.g., six months to a year) and have a stable revenue stream.

Business Plan: A solid business plan outlining the use of funds, projected growth, and repayment strategy can significantly enhance your chances of securing a loan.

Financial Statements: Providing accurate and up-to-date financial statements, including profit and loss statements, balance sheets, and cash flow statements, is crucial.

Purpose of the Loan: Clearly articulating why you need the loan—whether for business equipment financing, short-term business funding, or another purpose—can help lenders understand and approve your application.

Start by researching private money lenders in Florida. Look for those who offer the type of loan you need, whether it’s for business equipment financing, fast small business loans, or short-term business funding. Pay attention to their terms, interest rates, and customer reviews.

Having your documentation ready can streamline the application process. Here’s a checklist of commonly required documents:

Business Financial Statements: Profit and loss statements, balance sheets, and cash flow statements for the past six months to a year.

Tax Returns: Business and personal tax returns for the past one to two years.

Bank Statements: Recent business bank statements (typically the last three to six months).

Business Plan: A detailed business plan outlining the purpose of the loan, how the funds will be used, and how you plan to repay the loan.

Legal Documents: Business licenses, incorporation documents, and other relevant legal documents.

Most private money lenders offer online applications, making the process quick and convenient. Fill out the application form accurately, attach the necessary documents, and provide any additional information requested.

After submitting your application, follow up with the lender to ensure they have received all required documents and to check on the status of your application. Be prepared to answer any additional questions or provide further documentation if needed.